Research

Bitcoin Mining Market 2023 Outlook

May 4, 2023

Download the PDF version here: Bitcoin Mining 2023 Outlook

--

Bitcoin miners have been spared from the precipice by a welcome rally in BTC prices. As such, we felt it was an opportune time to review where we are now, how we got here, and our outlook for the future. While this is not an exhaustive list of industry fundamentals, this thought piece will provide a high-level overview of some key dynamics defining our investment thesis in 2023. Understanding the nuances of industry fundamentals is crucial to discerning market dynamics and allows us to assess better how we allocate capital across the opportunity set.

2022 Recap

2022 was undoubtedly a turbulent year for digital assets of all kinds. While the price of BTC was more resilient than most digital assets, the bitcoin mining sector was buffeted by perpetual headwinds. A plummeting Bitcoin price, soaring energy costs, and a steadily increasing hashrate all combined to create a perfect storm to squeeze mining margins. Market distress was further exacerbated by financial engineering (read: ASIC-backed loans) predicated on BTC’s steady - if not rising - value, an assumption that proved deadly for some operators. Many miners underwent major restructurings, and others filed for Chapter 11 bankruptcy. The strength of the 2022 headwinds has receded as the underlying BTC price rallies and market participants look to implement lessons learned from 2022. These conditions and opportunities presented by innovations in the space should ensure that 2023 will be an exciting year for Bitcoin mining.

Ongoing Headwinds: Margin Compression

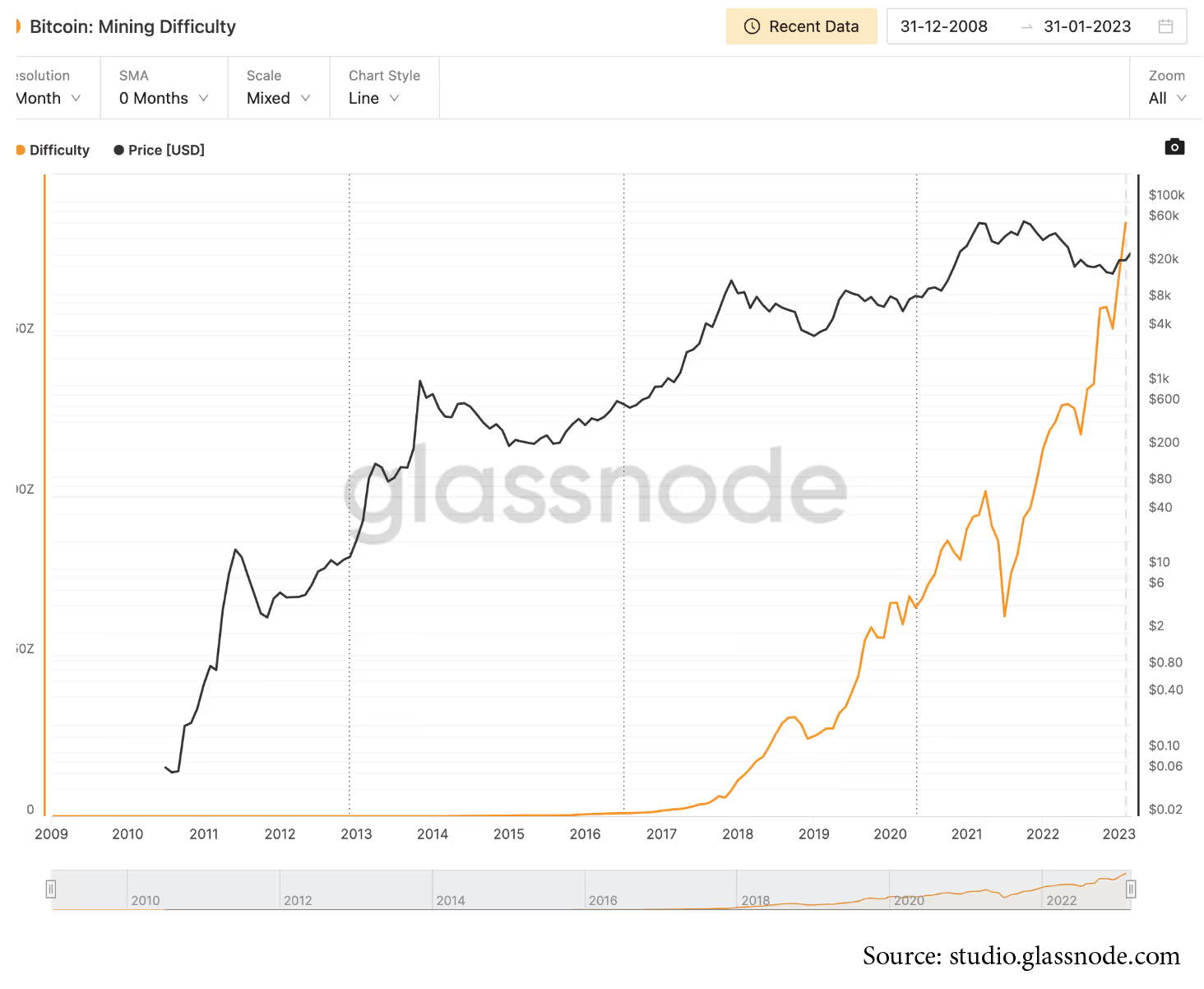

Network Hashrate

Searching for the ‘most important metric’ in any complex system is instinctive to simplify your understanding. Acknowledging that it is rarely just one metric that matters, the best proxy for the BTC mining sector is the Network Hashrate, which represents how much computing power is online. Bitcoin mining’s profitability is highly sensitive to the network hashrate. An individual miner’s market share is defined by the volume of hashrate deployed. Their profitability can be calculated on a formulaic basis corresponding to deployed hashrate compared to their costs - assuming a standard Full Pay Per Share (FPPS) payout model. Maintaining profitable margins requires a constant scaling of deployments to align with hashrate growth assuming costs are held constant.

Hashrate has continued to climb steadily higher since the summer of 2021. There has been some volatility with the lull in the summer of 2022 and brief periods of disruption as winter storms across the US lead to significant numbers of machines being turned off due to power outages and balancing the grid. The trend remains clear, hashrate continues to climb steadily upwards, squeezing mining margins as it goes as costs have - in general - been heading higher too.

The network will likely continue to see an uptick in hashrate in H1 as the latest generation ASIC miners are delivered per schedules agreed upon in 2022 and brought online. These new miners are more efficient in energy usage and the hashrate produced. However, the price premiums for the latest models are still significantly higher than the previous generation, making these less attractive to purchase in the prevailing conditions when considered on a Return-on-Investment lends. With a slower rate of additional hardware delivery scheduled for Q2/Q3, we believe the trend for network hashrate will continue to rise, but the velocity will moderate. As we approach Q4, the looming halving will rapidly be brought to the forefront of the conversation. In anticipation of the event, hashrate will likely start to pick up as participants are more willing to forego savings from older units and focus on the latest hardware with greater efficiency for the hashrate produced.

Cost of Capital

As 2022 progressed, the industry had to contend with capital provision moving from feast to famine. Public miners raised $750 million in Q1, a further $900 million in Q2 2022, and only $33 million in Q3. The cost of debt soared - if it was even available as lenders to the sector had their challenges to deal with - combined with rising costs, margin compression, and low cashflow liquidity, creating a toxic brew. This sent mining stock valuations plummeting and pushed the cost of capital even higher, leaving miners with sparse financing options. With weakening balance sheets and conditions bleak, many miners resorted to dilutive financing via at-the-market equity offerings in late 2022. The industry expected this would lead to consolidation, which has started occurring but at a lower cadence than we had anticipated. The cost of capital is expected to remain elevated in 2023, given the rise in interest rates and the regulatory pressures on the digital asset industry. Still, the good news is there is capital available once again.

Bitcoin Price

A key determinant for the industry will always be the price that Bitcoin - the sole good that is produced - can be sold. Although we have recently seen some positive price action in Bitcoin, there remains a high degree of uncertainty around broader macro conditions. The regulatory focus on the digital asset industry in 2023 presents additional friction that will likely cap near-term price appreciation. Given the tumultuous events of the previous year, it is anticipated that capital flows into digital assets will remain muted in 2023 compared to the prior year. The most positive event for the price of BTC remains the halving which is a 2024 event, so while we hope the recent price recovery continues, we expect more volatility as we are arguably still too early to expect to see the next major bull cycle.

Regulation

In 2023, regulation has shifted to the center of the conversation within the digital asset space, and the pressure shows no signs of abating. Regulators seek to take a more draconian stance on what is deemed inappropriate due to problems on display in the digital assets industry last year. Bitcoin mining is no stranger to scrutiny as several jurisdictions maintain a strict contrary stance, with some even seeking to implement mining bans. However, given many prominent market participants are publicly listed, have appropriate governance, and are subject to the SEC’s reporting requirements, mining is unlikely to be the focal point for additional regulations. As a result, mining activities should be able to avoid the brunt of the resurgence in regulatory clampdowns coming in 2023. However, recent noises on proposed taxation changes will be another headwind to the industry.

Supply

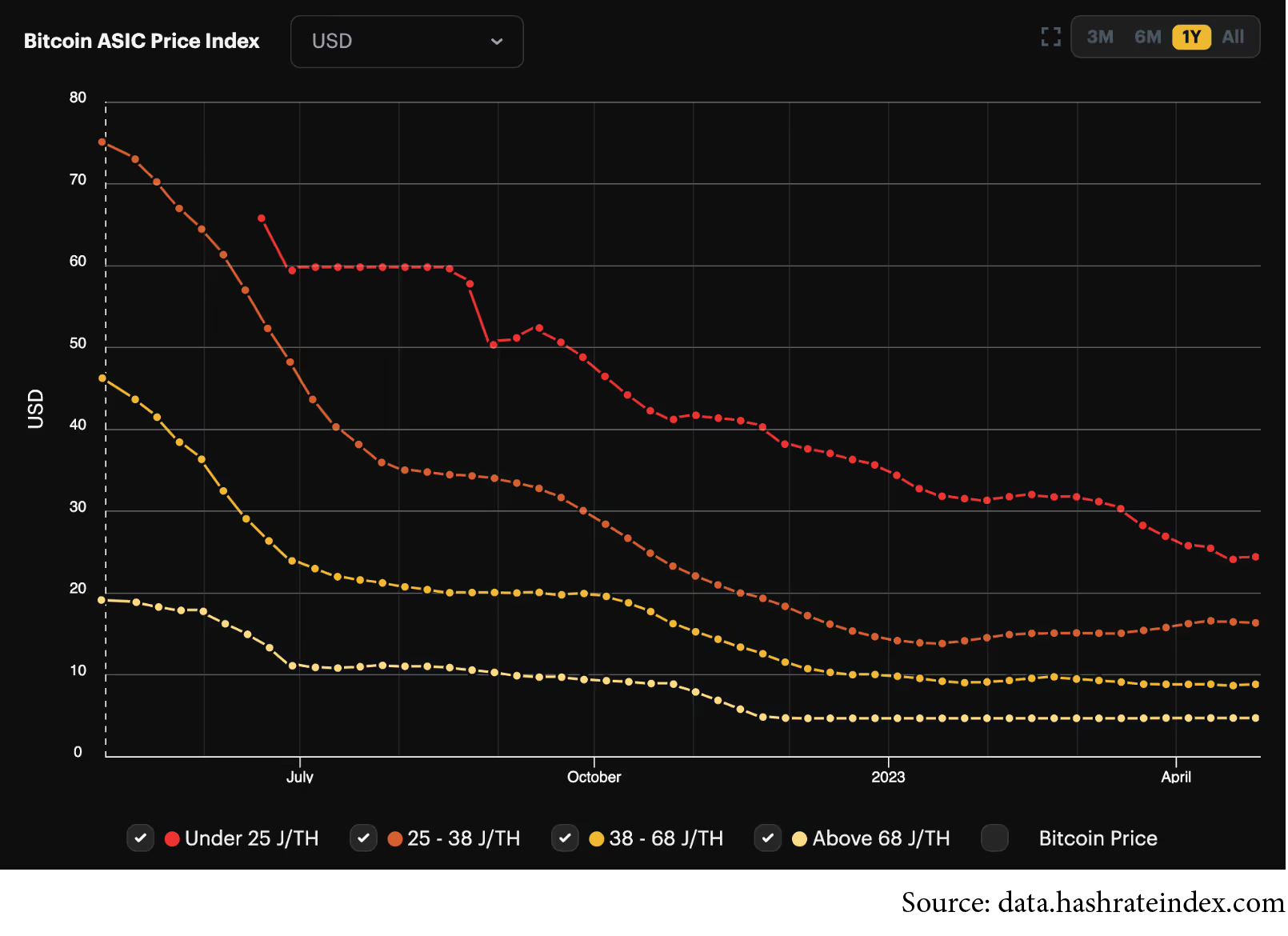

Every participant in the supply chain has obligations to fulfill, many of which were agreed upon under very different market conditions. Obligations from ASIC hardware manufacturers to chip producers mean machines continue to be manufactured despite relatively unattractive economics. Dominant players are subsequently sitting on extensive inventories, despite hardware prices being ~90% YoY. In addition, market distress and bankruptcies have led to many creditors sitting on ample supplies of machines where participants have defaulted on hardware-backed debt.

Present Day: Survival of the Fittest

Deleveraging

One of the critical lessons learned throughout 2022 was a story as old as finance - leverage amplifies returns in both directions. With most large miners relying on undiversified revenue streams coupled with steep debt terms, the new backdrop of tighter fundamentals has left many companies unable to meet interest obligations because of insufficient operational cash flows. As a result, many loans were underwater, and we saw a heightened risk of bankruptcy, with several high-profile companies filing. The term on most hardware-backed loans comes due before March 2024, given the uncertainty of industry performance post halving. As a result, companies face not only the burden of interest expense but also principal repayments, which heavily erodes free cash flow. Some participants continue to look at financing growth via traditional debt structures. Still, the days of easy monetary conditions and heavy leveraging via hardware-backed debt are most likely behind us for the foreseeable future. As a result, the industry has shifted focus to improving balance sheet health requiring substantial deleveraging.

A low debt burden is a key indicator of Company health in a rising interest rate environment. Market participants with solid balance sheets and sufficient runway are best positioned to weather the current market, manage the halving, and gain from consolidation ahead of the next bull cycle. As hashrate directly correlates to market share, the name of the game in 2023 is survival, and those who last will reap the long-term benefits.

Restructuring of Cost Models

Energy prices are a core determinant of the profitability of a Bitcoin mining operation. As a result, the energy price inflation seen in 2022 hit the mining industry hard. Participants were already facing razor-thin margins from lower Bitcoin prices and increasing hashrate coming online, leaving them heavily motivated to reduce their cost burden via more sophisticated energy cost management.

Fixed-term, low-cost Power Purchase Agreements (PPAs) are a compelling low-risk route, providing comfort for investors and complemented with curtailment credits, can provide diversified revenue streams. Low-cost, fixed-term contracts also offer more flexibility as wider margins mean miners do not have to use the latest generation hardware to retain sufficient profitability. The challenge is to have the prescience to secure one before prices rise.

Beyond the classic fixed-term PPA, many miners are starting to incorporate more sophisticated strategies leveraging energy mixes with lower price volatility, participating in demand response programs, and engaging in hedging/trading strategies. More sophisticated energy strategies do, however, require the appropriate expertise within the team. Energy market expertise has become an undeniable advantage within management teams. Those miners with dedicated energy teams or management with commodities backgrounds are much better positioned to leverage price volatility for better risk management.

In addition to securing cheaper power, miners facing higher cost burdens will likely continue to seek efficiency gains by deploying the latest mining hardware technologies, management software, and immersion cooling.

Vertical Integration

2022 saw some of the largest hosting providers file for bankruptcy, highlighting the risk of hosting models and the importance of vertical integration. While asset-light models have often been favored and are particularly attractive in bull runs, Core Scientific and Compute North’s recent events shed light on the risk in such models. As a result, most miners are focused on more vertically integrated strategies in the future. Even those looking to keep the asset-light approach know the importance of direct relationships with energy providers, particularly in a high-cost energy environment. Integration of multiple businesses via M&A to diversify geographies and revenue streams has already begun to pick up in 2023. This theme, we anticipate, will continue as participants try to reduce any frailties in their business models.

Timing is everything

If 2022 was the year of capitulation, then we anticipate the story of 2023 will be consolidation. There is a vast selection of consolidation opportunities across assets, sites, and operators. Those players who are well positioned to weather the bear market still face margin pressure from the increasing hashrate and the looming halving - although recent price action in the underlying Bitcoin price is most welcome. Consolidation ahead of the halving will be essential for many miners to achieve scale sufficient to maintain healthy margins and stay in the game. Opportunities to scale are expected to remain top of mind. The majority of the market is conscious of the past year’s mistakes, especially as they continue to take delivery of machines ordered in prior times. So miners are selective with the purchase opportunities and often prefer distressed asset purchases over traditional M&A. With the recent announcement of the merger between Hut8 and USBTC, Galaxy Digital’s acquisition of Argo’s Helios facility, and CleanSpark’s purchases of Sandersville and Washington facilities, the industry recognizes the significant economies of scale gained by merging with or acquiring competitors. We are seeing the beginnings of a new wave of consolidation and will likely see a lot more activity across the industry throughout 2023.

On the horizon: Innovation and Disruption

Beyond the broader mining market dynamics, we foresee four high-impact themes offering the potential for disruption in the medium term.

ASIC Production

The ASIC market is dominated by two leading players, Bitmain and MicroBT. Reindustrialization in the US, the CHIPS and Science Act, juxtaposed with deglobalization themes - as labor and input price arbitrage erode - leaves room for disruption within the ASIC production space. The market structure and innovations in ASIC technologies relating to immersion cooling and new chip design suggest that the industry could be ripe for disruption. Companies such as Intel, who focus on manufacturing chips over the entire mining rig leveraging innovation in immersion cooling and other efficiency-improving technologies, will open the hardware market up for new players. Given the high friction costs and CAPEX-heavy model required, we may have to wait until the next bull market to see more defined market penetration, but it will remain a space to watch.

Efficiency Optimization

Given the need to control costs in the volatile energy environment that we find ourselves in, efficiency gains are top of mind for mining firms. The market for management software to optimize energy usage and fleet management is fragmented, with most miners using software solutions developed in-house with varying degrees of sophistication. There is a significant opportunity for disruption within this market via white-labeled solutions or third-party leasing by those who have developed more sophisticated solutions. Software solutions and other revenue-generating strategies also contribute to revenue diversification which is increasingly a priority across the market.

Derivatives

Bitcoin is not a yield-bearing asset. While its rigid network structure makes it compelling from a network security and risk standpoint, the inability to successfully deploy applications and yield-bearing instruments on top of the blockchain means there is still tremendous value to be extracted. Some platforms and protocols have attempted to do so - Stacks & Lightning being the most prominent - but there is still huge untapped potential.

In many ways, Bitcoin’s Proof-of-Work structure mirrors traditional commodity mining. On that basis, derivative opportunities relating to hashrate become compelling instruments to bridge the gap between digital assets and traditional finance markets. Having watched this space develop over the past 18 months, we are clearly in the early stages. However, there is a significant value opportunity here as more sources of capital start to seek risk-managed exposure to digital assets in a much stricter regulatory environment. Instruments that can be standardized and look closer to the variance swaps found on Wall St. are likely the more compelling products in the medium term.

While we are starting to see more structured products appear, they remain more compelling from the seller’s perspective. Gaining volumes on the buy side has remained difficult given the fundamentals of supply overhang and mixed crypto appetite amidst the present regulatory clampdown - as a result, it is hard to be long hashprice currently. A liquid derivatives market can help miners to diversify their revenue further and stabilize price swings which should further capital inflows, so we remain supportive of these developments.

ESG

Another energy consideration that is becoming increasingly important is the interplay between mining deployments and the grid. Recent winter storms wreaking havoc for residents across US states who are not accustomed to such extremities have highlighted the importance of miners’ cooperation with Grid Providers such as ERCOT. Working proactively with localized grid providers can yield a more stable grid service, where large miners act as a grid buffer and offer load-balancing capabilities. This provides miners with a more diversified revenue stream, aligns incentives, and creates a more stable grid for all users. Aligning incentives with third parties is a fundamental aspect of ESG considerations and will become increasingly important as regulators take a more stringent stance.

Wrapping Up

With an eventful year behind us, continued headwinds, consolidation, and new innovation in the space, we are watching Bitcoin mining developments for how best to deploy capital. Based on industry fundamentals and broader macro dynamics, 2023 will be a pivotal year for bitcoin mining as the industry finds its feet ahead of the 2024 halving. All in all, this will be an exciting space to watch.

DISCLAIMER

The content of this document is for information purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this document constitutes a solicitation, recommendation, endorsement, or offer by Hivemind Capital Partners, LLC (“Hivemind”) or any third-party service provider to buy or sell any securities or other financial or non-financial instruments in this or in in any other jurisdiction in which such solicitation or offer would be unlawful under the laws of such jurisdiction. Nothing in this document constitutes professional and/or financial advice, nor does any information in this document constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. All content in this document is information of a general nature and does not address the circumstances of any individual or entity.