Articles

Stablecoins: 10 Years of Growth and the Road Ahead

Kayla Phillips

November 21, 2024

This month, Tether celebrates 10 years since the launch of USDT, today’s largest stablecoin with a 67% market share. A decade in the making, stablecoins have ballooned to a $195B market with volumes growing 17% YoY.

Initially created to provide on-chain liquidity for crypto trading and defi, stablecoins have since become embedded in emerging economies as an inflation hedge and remittance medium and are now being adopted by the largest financial institutions in the world to facilitate efficient global money movement and settlement by ‘moving value at the speed of the Internet.’ We are moving towards a future where stablecoins and blockchains underpin our open, global financial infrastructure.

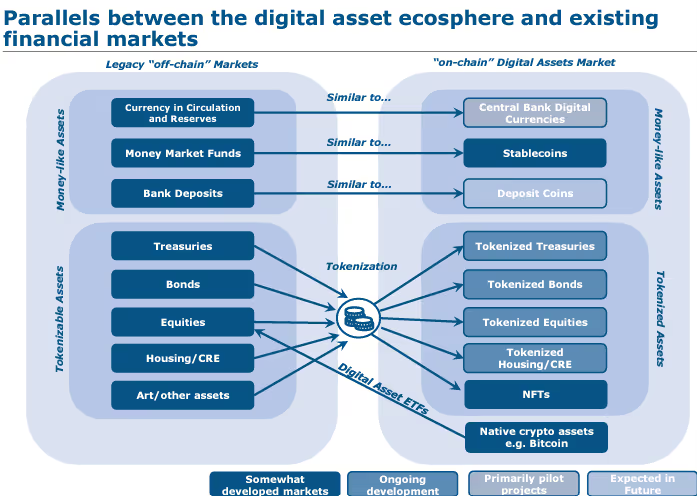

This means that stablecoins are approaching the critical mass where they are becoming too big to ignore. Financial institutions and fintech firms are investing more heavily in this space, with PayPal, Ripple, Revolut, and others launching their own stablecoins, while BlackRock, Franklin Templeton, etc., are tokenizing funds to bring greater liquidity on-chain to enable the launch of new stablecoin and real-world asset (RWA) products. Regulators worldwide are also rolling out new stablecoin regulations, providing guidelines to support mainstream adoption and incorporating these products into their financial systems and economies. The EU, UK, Singapore, UAE, and Hong Kong are among the countries that have recently implemented their own stablecoin regulation. Notably missing from this list is the US, where Congress has dragged its feet in this process, but legislation has growing bipartisan support.

We believe that stablecoins are here to stay, and the market is growing in terms of both adoption and innovation. In terms of innovation, there are 4 main stablecoin categories today: Fiat-backed (primarily by USD), Commodity-backed (by gold, silver, oil, etc), Crypto-backed (by a basket of crypto assets like BTC & ETH), and Algorithmic (backed by an algorithm). However, more recently, we have seen innovation and expansion across several dimensions:

- Yield-bearing stablecoins: These stablecoins generate yield from either RWAs (primarily T-Bill yield) or from defi (primarily staking yield or delta-hedged futures funding rates).

- Geographic: Fiat-backed stablecoins pegged to a currency other than USD and/or benefit from a regulatory moat or regulatory arbitrage in a particular jurisdiction.

We expect continued growth across these dimensions as more money flows into the space and more jurisdictions provide regulation.

We believe that there are four key areas to watch for in the near term:

- US regulation, finally.

Though the US has resisted passing comprehensive stablecoin legislation to date, it plays a central role in the fast-growing, $180B stablecoin market that is becoming too big for it to ignore. More than 95% of the stablecoin market is made up of USD-pegged stablecoins, the US Treasury attributes stablecoin growth to increasing demand for T-Bills ($120Bin stablecoin collateral is invested in Treasuries), and people all over the world are now holding stablecoins as digital USD equivalents. The growth of the Eurodollar system for offshore USD outside of the control of the US Government led to uncomfortable situations into and through the Great Financial Crisis. It is anticipated that Congress will soon want to oversee the issuance and reserve-backing of USD-pegged stablecoins to avoid being blindsided.

- Expansion --> convergence of public stablecoins.

In recent months, quite a few new stablecoins have been announced, with others rumored. Most of these will be open-loop stablecoins, meaning that they will circulate freely on public markets for B2B or B2C use cases and will aim to chip away at Tether and Circle’s market share. We expect that the current market expansion will ultimately converge around a select few dominant players – existing leaders Tether and Circle, plus a couple of others that distinguish themselves via distribution (i.e., PYUSD), geography (i.e., RD), or protocol/token mechanics (i.e., USDe).

- The rise of closed-loop stablecoins.

While open-loop stablecoins have made more headlines, we expect significant growth in closed-loop stablecoin usage. These stablecoins will power more internal operations at financial institutions, fintech firms, and enterprises to improve efficiencies (cross-border money movement and settlement) and user experiences (new forms of ‘in-store currency’ and loyalty programs). Indeed, this is a natural evolution of some firms' internal ledgers for moving value between various stakeholders.

- Tradfi institutions increasing investment in stablecoins and RWASs.

Over the last few years, traditional financial institutions have invested small pockets of money into R&D and pilot projects for stablecoins and adjacent categories of tokenized RWAs. As the pace of innovation and adoption accelerates, institutions are allocating more funding to these efforts to grow pilot projects into larger-scale developments within their organizations. We expect this funding to continue to increase in future years.

We believe that leading stablecoin projects will check at least some of these boxes:

- Prioritization of regulatory compliance and licensing rather than creative workarounds to avoid it. Additionally, transparency, proof of reserves, and bankruptcy remote structures are becoming expected by retail and institutional holders alike.

- Alignment with exchanges. Stablecoins that strategically align with exchanges (i.e., Coinbase-USDC, Hashkey-RD,Kraken-USD0) have an advantage over those that do not, as exchanges can support stablecoin distribution by facilitating multi-chain trading activity.

- Stablecoin design that simplifies and improves the user experience. For example, a solution we believe would have a strong market fit would be where a single stablecoin asset is held in a single account (wallet/payment infrastructure built to support it) that is yield-generating and easily spendable – with any other complexities or mechanics abstracted away from the user. Essentially, it is a high-yield checking account enhanced by crypto, where holding a stablecoin enables a user to passively earn income and easily spend it at any digital or physical merchant worldwide.

- Stablecoin infrastructure that paves the way towards a future global financial system run on stablecoins and blockchains. Stablecoin orchestration tools that make it easy and seamless to swap between different stablecoins and different fiat currencies are an example of this. Bridge, a leading company in this space, made headlines last month when it was acquired by Stripe for $1.1B. This was both Stripe’s largest acquisition and the crypto industry’s largest acquisition to date.

Our recent investment in Round Dollar (RD) Technologies meets each of the above criteria. RD has taken a regulatory-first approach as a front-runner to receive Hong Kong’s coveted new stablecoin license and has strategically aligned with Hashkey to support its distribution. Regarding its stablecoin design and infrastructure, RD has abstracted away its technical architecture and B2B payment rails to simply offer corporate customers a multi-currency business account with fast, cost-efficient cross-border B2B payments with instant settlement.

In summary, the years of work the crypto industry has invested in stablecoin progress and adoption have finally led us to the current inflection point, where stablecoins move beyond crypto-native and emerging markets usage to reach mainstream adoption on a global scale. The Hivemind team could not be more excited about the open global financial system we envision for the future and will continue to invest in the solutions that drive us closer to realizing this potential.