.svg)

Articles

Stablecoins and Tokenization: the rails are being built in public

Richard Skeet

March 19, 2026

If Q4 reminded investors that price can be volatile and positioning fragile, it also reinforced a quieter truth: the settlement rails of the digital asset system kept strengthening regardless of market direction.

Stablecoins and tokenized financial assets continued to grow, integrate, and formalize even as risk appetite fell. That divergence matters. It suggests that while speculative layers of the market remain cyclical, the monetary and collateral infrastructure layers are becoming structural.

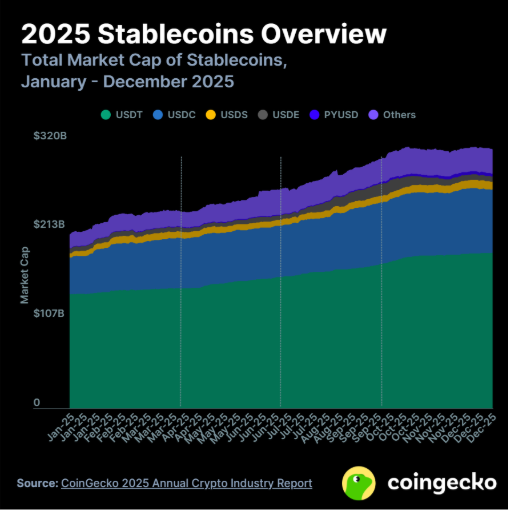

Stablecoins finished 2025 at a record scale. CoinGecko estimates total stablecoin market capitalization reached roughly $311B, up close to 50 percent year on year, even after segments of the synthetic and high-yield stablecoin complex deleveraged sharply following October’s market stress. The composition of that supply also continued to shift toward more regulated, fiat-backed models with clearer reserve disclosures and policy alignment. In other words, the market is converging toward stablecoins that look less like experiments and more like narrow digital banks or money market conduits.

This evolution is not accidental. Policy frameworks are catching up to usage. Hong Kong’s stablecoin licensing regime went live in August 2025, establishing a formal supervisory structure for fiat-referenced stablecoin issuers, with the HKMA signaling its intention to issue the first licenses in 2026. In the United States, federal stablecoin legislation advanced materially, defining reserve standards, custody rules, and supervisory expectations for payment stablecoins. Across jurisdictions, the direction of travel is similar. Stablecoins are being pulled into the regulated perimeter, not pushed out of the system. That is typically what happens when financial technology demonstrates product-market fit.

From an investment perspective, stablecoins should be viewed less as “crypto assets” and more as digital settlement infrastructure. They reduce friction in moving dollars across platforms, time zones, and counterparties. They enable atomic settlement in trading and lending. They act as on-chain collateral. They allow programmable payment logic. They are already widely used in crypto-native markets, but their greater significance is that they make traditional financial activity easier to express on-chain. In that sense, they are closer to messaging and clearing rails than to speculative tokens.

Tokenization extends this logic from money to assets. Through 2025, tokenized Treasury bills, money market funds, and other yield-bearing instruments moved from pilot stage toward scaled products. Large asset managers and banks expanded tokenized fund offerings, while on-chain fund structures grew in both assets and transaction counts. BlackRock’s on-chain fund products, Franklin Templeton’s tokenized money market fund, and bank-led tokenized deposit and fund initiatives like the recently announced Strategic Partnership between Hivemind and CPIC illustrate the direction: traditional instruments, expressed as programmable wrappers, settled on-chain.

The practical advantages are operational rather than ideological. Tokenized funds can settle faster, support fractional ownership, embed compliance logic, and integrate directly with on-chain collateral and lending systems. Transfer restrictions, investor eligibility, and reporting logic can be expressed at the token layer. This reduces back-office reconciliation and creates cleaner audit trails. None of this requires abandoning regulations. In fact, most successful tokenization efforts are explicitly regulation-forward. The point is not to escape the system but to modernize its plumbing.

There is also a macro dimension that is increasingly difficult to ignore. Stablecoins and tokenized Treasury products create new demand channels for short-duration government debt. When fiat-backed stablecoins grow, their reserves are typically held in cash and short-term sovereign instruments. When tokenized Treasury funds grow, they directly intermediate government bills into digital wrappers. Several macro researchers have argued that this dynamic effectively creates a new distribution channel for sovereign collateral, one that is API-driven rather than broker-driven.

This is where the decentralization lens remains useful. Public blockchains provide a neutral, shared ledger on which these instruments can exist without being tied to a single platform operator. The tokenization layer can be compliant and permissioned, while the settlement layer remains open and verifiable. That separation is powerful. It allows innovation and control to coexist. As we have written before, decentralization is best understood as a resilience feature. It reduces dependence on single operators and closed databases while still allowing regulated actors to build controlled applications on top of them.

Importantly, none of this means the path is frictionless. Stablecoin failures, reserve questions, and design flaws have already produced losses in earlier cycles. Tokenization projects can overpromise and underdeliver. Liquidity can fragment across platforms. Legal enforceability must be tested, not assumed. Just as with base-layer protocols, the work is hard, and the trade-offs are real. But the direction is consistent. Financial assets are becoming more programmable, more granular, and more directly integrated with settlement logic.

We view stablecoins and tokenization as infrastructure trends rather than trades. They increase the usefulness of on-chain systems, deepen liquidity pools, and connect digital assets to traditional collateral markets. They also reinforce the investment case for neutral settlement layers like Ethereum, where much of this activity is concentrated, and for policy-compliant on-chain frameworks more broadly. Put simply, the rails are being built in public. Price cycles will come and go, but payment and collateral infrastructure, once adopted, rarely gets unbuilt.

--

DISCLAIMER: All views expressed are Hivemind’s own views. The information provided herein has been produced and issued by Hivemind Capital Partners UK LLP and/or Hivemind Capital Partners LLC (“Hivemind”) and is being provided for informational purposes only. This document is not to be distributed or reproduced in any way. This document does not constitute or contain an offer to purchase or sell securities. This document is confidential and intended for the person to whom this was delivered. If you have not received this document from Hivemind you are hereby notified that you have received it from a non-authorized source and you are prohibited from reading, using, retaining, disseminating or copying this material without the prior express written consent of Hivemind. Neither Hivemind nor any of its affiliates or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein or any other written or oral communication transmitted or made to the recipient. The information contained in this document is current as of the date indicated, and Hivemind undertakes no obligation to update, modify or amend this document or to otherwise notify a reader in the event that any matter stated herein changes or subsequently becomes inaccurate.

This document has not been compiled, reviewed, or audited by an independent accountant. Past performance should not be construed as an indicator of future results, and there can be no assurance that historical trends will continue. This document does not include information regarding each investment or investment strategy pursued by the Funds. References to investments included herein should not be construed as a recommendation of any particular investment.

Certain information contained herein may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof, other variations thereon or comparable terminology. All such forward-looking statements are solely statements of opinion, and there is no assurance that they will be predictive of actual events.