Articles

Perpetuals, basis, and liquidity: where price discovery now lives

Richard Skeet

April 16, 2026

One of the most important structural shifts in digital asset markets is where price discovery actually happens.

Spot markets still set reference prices, but risk transfer has decisively shifted toward derivatives, especially perpetual futures. Q4 made that clear again. The largest moves, forced liquidations, and liquidity air pockets were driven less by spot selling and more by leveraged positioning resetting through perpetual swap markets. Understanding crypto now requires understanding perps, funding, and basis, not just token narratives.

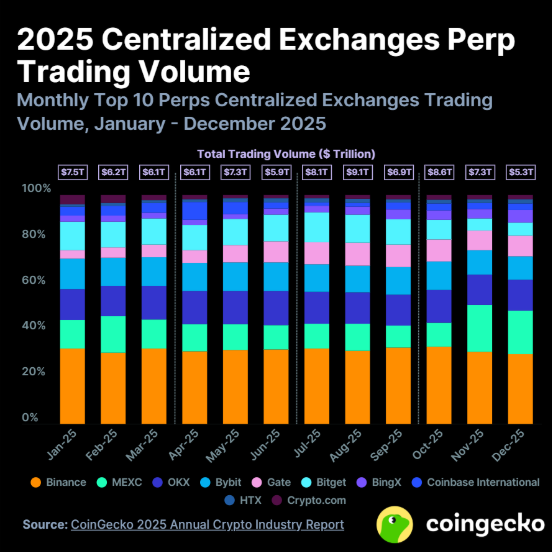

Perpetual futures volumes reached a historic scale in 2025. CoinGecko estimates that centralized perpetual venues processed more than $86T in notional volume across the year, up strongly year on year, with decentralized perpetual venues also expanding rapidly into multi-trillion-dollar annual volume. Even though Q4 risk appetite fell, derivatives activity remained elevated, with centralized perp volume still above $20T for the quarter and decentralized perp share reaching record levels. In practical terms, more risk is now expressed through leverage-adjustable instruments than through outright spot ownership.

This matters because perpetual futures embed a continuous positioning signal through funding rates. When longs dominate, funding turns positive, and longs pay shorts. When shorts dominate, the sign flips. That mechanism turns positioning imbalance into a real-time cost. In trending markets, persistent positive funding can signal crowded longs and unstable equilibrium. In stressed markets, funding can invert violently as positioning unwinds. Q4’s October dislocation clearly showed this dynamic, with rapid funding resets and liquidation cascades amplifying price moves beyond what spot flows alone would likely have produced. Funding is no longer just a trader's detail. It is a microstructure indicator.

Basis, the spread between futures and spot has also matured into a usable structural signal. In strong bull phases, futures often trade at a premium to spot, reflecting demand for leveraged exposure. In risk-off phases, that premium compresses or turns into a discount. The compression of basis in Q4 coincided with declining leverage appetite and tighter liquidity conditions. For allocators and systematic traders, basis regimes increasingly function like credit spreads in traditional markets. They are a barometer of risk demand and balance sheet availability, not just a pricing curiosity.

Another notable shift is venue mix. Decentralized perpetual exchanges gained share again in 2025, both in absolute volume and as a fraction of total derivatives activity. CoinGecko reports that decentralized perp volumes reached record quarterly levels in the second half of the year. This does not mean centralized venues are disappearing. It does mean liquidity is fragmenting across execution environments with different margin rules, liquidation engines, and collateral types. That fragmentation can increase resilience but also produce cross-venue dislocations, in which price and funding temporarily diverge before arbitrage capital reconnects them.

From a portfolio management standpoint, this evolution changes how liquidity risk should be framed. Liquidity is no longer just about order book depth on spot exchanges. It is about liquidation geometry across leveraged venues. When positioning is crowded, and margin thresholds are tight, small price moves can trigger mechanical selling through liquidation engines. Those flows are insensitive to fundamentals. They are rule-based and immediate. The October Q4 liquidation wave is a recent reminder that leverage transforms volatility from a statistic into a mechanism.

There is also a reflexive loop between derivatives and spot through collateral. Many leveraged positions are margined in stablecoins or major tokens. When volatility rises, margin calls create demand for collateral or prompt forced sales. Stablecoin flows, perp liquidations, and spot volatility are therefore linked. This is one reason why stablecoin supply and exchange balances are increasingly useful context indicators alongside price and volume.

None of this makes derivatives markets inherently unhealthy. On the contrary, they are a sign of market maturation. Traditional commodities, rates, and equity index markets are all highly derivative-heavy in terms of risk transfer. But it does change how digital asset volatility should be interpreted. Moves are not always narrative-driven. Many are position-driven. The difference matters for timing, sizing, and patience.

Our takeaway is not that leverage should be avoided entirely, but that it must be respected as a first-order driver of outcomes. When perp volumes dominate and funding is extreme, markets become more path-dependent and less forgiving. When the basis is compressed and funding neutral, risk transfer is more balanced, and price discovery is more orderly.

As the market continues to professionalize, edge increasingly comes from understanding how the plumbing behaves under stress, not just what the story is at the top.

--

DISCLAIMER: All views expressed are Hivemind’s own views. The information provided herein has been produced and issued by Hivemind Capital Partners UK LLP and/or Hivemind Capital Partners LLC (“Hivemind”) and is being provided for informational purposes only. This document is not to be distributed or reproduced in any way. This document does not constitute or contain an offer to purchase or sell securities. This document is confidential and intended for the person to whom this was delivered. If you have not received this document from Hivemind you are hereby notified that you have received it from a non-authorized source and you are prohibited from reading, using, retaining, disseminating or copying this material without the prior express written consent of Hivemind. Neither Hivemind nor any of its affiliates or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein or any other written or oral communication transmitted or made to the recipient. The information contained in this document is current as of the date indicated, and Hivemind undertakes no obligation to update, modify or amend this document or to otherwise notify a reader in the event that any matter stated herein changes or subsequently becomes inaccurate.

This document has not been compiled, reviewed, or audited by an independent accountant. Past performance should not be construed as an indicator of future results, and there can be no assurance that historical trends will continue. This document does not include information regarding each investment or investment strategy pursued by the Funds. References to investments included herein should not be construed as a recommendation of any particular investment.

Certain information contained herein may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof, other variations thereon or comparable terminology. All such forward-looking statements are solely statements of opinion, and there is no assurance that they will be predictive of actual events.